If you’ve been watching the news lately, you’ve probably heard a lot about inflation. Rising prices, cost-of-living pressure, and interest rates going up can feel like the odds are stacked against you.

But here’s something that might surprise you: if you have a fixed-rate mortgage, inflation could quietly be working in your favour. In fact, it might be one of the most underrated financial advantages everyday Australians already hold — without realising it.

In this article, we’ll explain exactly how it works, why it matters, and what it means for your financial future.

The short version: If you have a fixed-rate mortgage, inflation is quietly shrinking your real debt while your home’s value climbs. You’re building equity from both ends — without doing a thing.

First, let’s understand what inflation actually does to debt

Inflation means the purchasing power of money goes down over time. A dollar today buys less than a dollar did five years ago.

Most people think about that in terms of groceries or petrol. But here’s the part that doesn’t get talked about enough: inflation does the same thing to your debt.

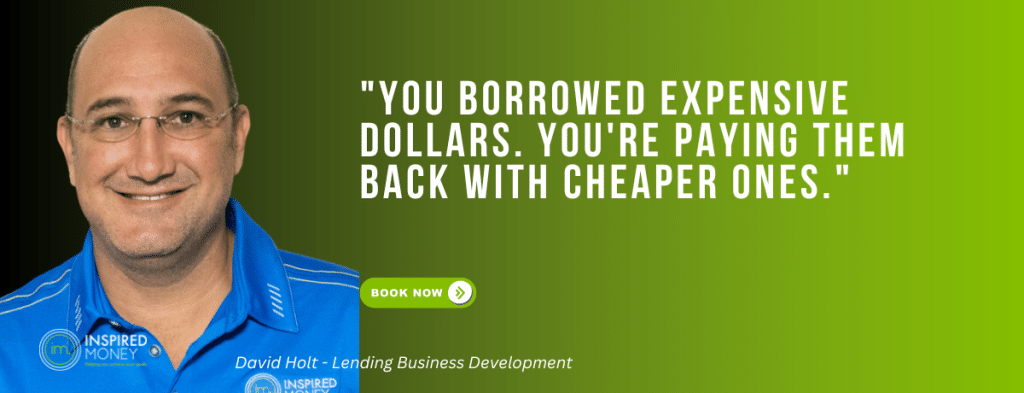

The $400,000 you borrowed five years ago is still $400,000 on paper. But in real terms, in terms of what that money actually buys, it’s worth less today. You borrowed expensive dollars. You’re paying them back with cheaper ones.

That’s not a loophole. That’s just how money works.

Why a fixed rate makes this even more powerful

When your interest rate is fixed, your repayment stays the same, month after month, year after year. $2,200 a month today is still $2,200 a month in five years.

But here’s what changes: your income. Over time, wages tend to rise (at least roughly) with inflation. Which means that fixed $2,200 repayment takes up a smaller slice of your household budget as the years go by.At the same time, your property, a real, physical asset, tends to reprice upward with inflation too. So while your debt stays the same in dollar terms, your home’s value climbs.

The result? You’re building equity from two directions at once. Your asset goes up. Your real debt burden goes down.

The history that proves it works

This isn’t just theory. History has shown it playing out in dramatic fashion.

In the late 1970s, an oil crisis triggered a severe inflationary shock across the Western world. In the United States, mortgage rates eventually peaked at around 18%. New homebuyers were locked out of the market, they simply couldn’t afford to borrow.

But the homeowners who had locked in fixed rates of 8–9% a few years earlier? They were sitting on something extraordinary. Their repayments hadn’t changed. Their home values had roughly doubled. And the real value of their debt had been cut nearly in half by inflation.

New buyers faced 18% rates. Existing fixed-rate holders were quietly building wealth, just by holding on.

What this means for Australian homeowners right now

In Australia, our fixed-rate terms are shorter than in the US — typically 2 to 5 years rather than 30. That does limit the effect compared to what an American homeowner might experience. But the principle still applies, especially for those who locked in low fixed rates during 2020–2021.

And more broadly, it’s a reminder that your home loan isn’t just a cost. Used wisely, it’s a financial tool, one that can work with inflation rather than against you.

Warren Buffett has called the fixed-rate mortgage “an incredible instrument.” Ray Dalio, one of the world’s most respected macro investors, points to hard assets financed with fixed nominal debt as one of the few genuine wealth preservation strategies in inflationary environments. That’s a rare consensus from two people who rarely agree on anything.

Right now, more than 30% of Australian mortgage holders are considered at risk, which makes getting your loan structure right more important than ever.

Your next step

You don’t need to be a sophisticated investor to benefit from this. What you do need is clarity on where your mortgage currently sits and whether your current structure is actually working for your goals.

A good starting point: review your home loan this month. Is your rate fixed or variable?

When does it expire? Is your current structure aligned with where you want to be in five years?

If you’re not sure, that’s exactly what a mortgage review conversation is for. Our team can help you look at the full picture, not just the rate, but how your debt fits into your broader financial life.

Getting your mortgage right isn’t just about finding the lowest rate. It’s about understanding how your biggest liability can also be one of your most powerful financial assets. And sometimes, the news that feels scary on the surface is actually working harder for you than you think.

This article contains general information only and does not take into account your personal financial situation or needs. Before acting on this information, consider whether it’s appropriate for you and seek advice from a licensed financial adviser or mortgage broker.