If you’ve ever asked how much super should I have at 40 Australia — you’re not alone. It’s one of the most Googled superannuation questions in the country, and for good reason. Your 40s are a pivotal decade. You’re likely earning more than ever before, the kids might be getting older, and retirement — while still 20-plus years away — is starting to feel like a real thing you should probably think about.

So here’s the direct answer: according to widely cited industry benchmarks, a 40-year-old aiming for a comfortable retirement should ideally have around $168,000 in superannuation. But here’s what’s equally important to know — most Australians aren’t there yet, and that doesn’t mean you’ve missed the boat. Not even close.

How Much Super Should I Have at 40 in Australia? What the Benchmarks Say

To understand super targets, it helps to start at the finish line and work backwards.

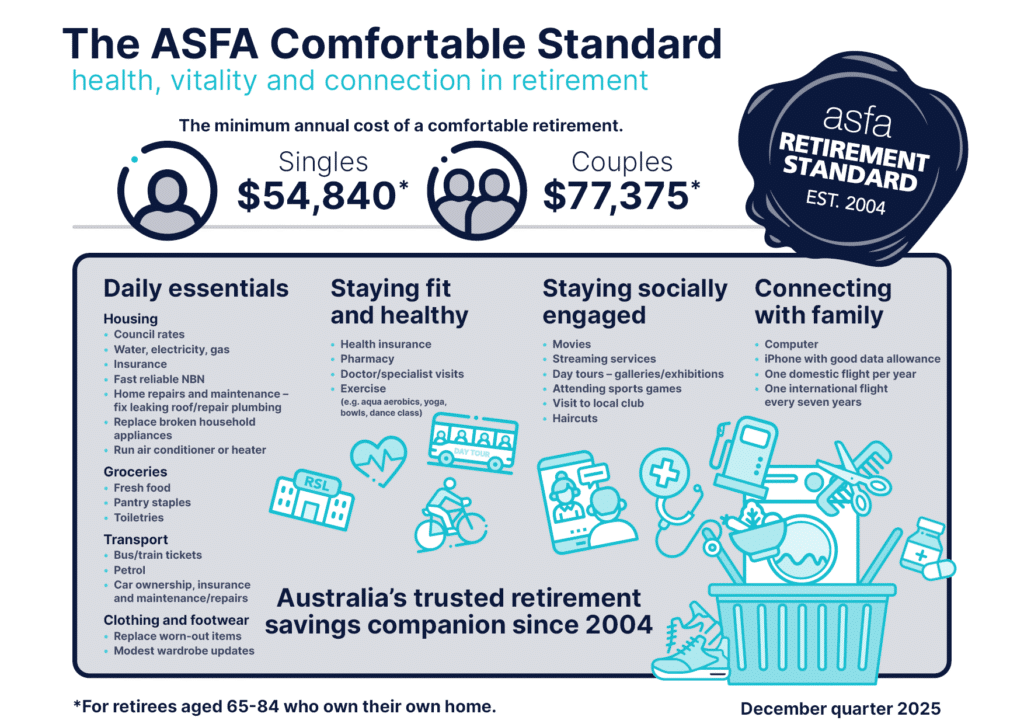

The ASFA Retirement Standard — published by the Association of Superannuation Funds of Australia — is the most widely used measure of how much income Australians need in retirement. As at late 2025, a comfortable retirement requires approximately:

- $54,240 per year for a single person

- $76,505 per year for a couple

To fund that lifestyle from age 65, ASFA estimates you’d need a lump sum of roughly $630,000 for singles and $730,000 for couples — on top of the part Age Pension that most retirees are eligible for.

A modest retirement (better than the Age Pension, but enough for the basics) requires around $35,199 per year for singles, with a much smaller lump sum target of $110,000.

So, working backwards from the comfortable figure of $630,000 at age 65, and assuming consistent investment returns and ongoing employer contributions, industry estimates suggest that a 40-year-old single person needs around $168,000 in super today to stay on track. That figure shifts depending on your income, your super fund’s investment returns, and whether you’re single or part of a couple — but it’s a useful starting point.

A note on these figures: All ASFA targets assume you own your home outright by retirement and are eligible for a part Age Pension. Your personal target may differ significantly from these benchmarks. This is where tailored financial advice becomes valuable.

Where Most 40-Year-Olds Actually Stand

Here’s where the honest conversation gets a little uncomfortable — but stick with us, because there’s a genuinely encouraging point at the end of it.

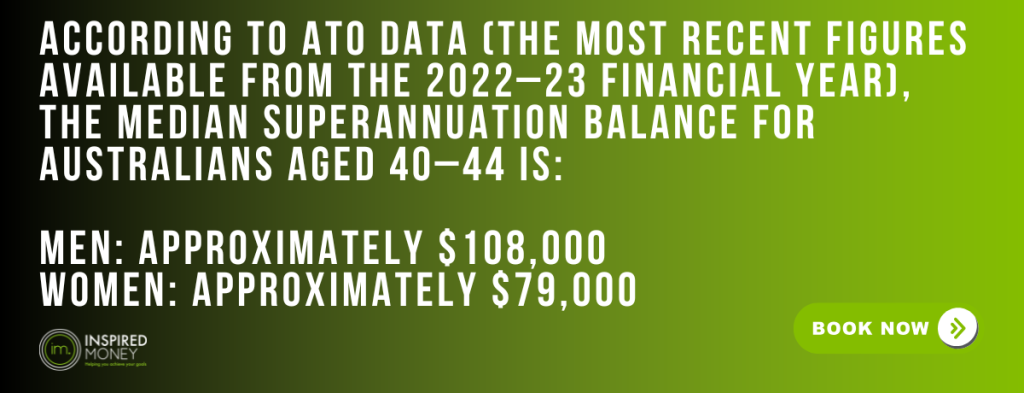

According to ATO data (the most recent figures available from the 2022–23 financial year), the median superannuation balance for Australians aged 40–44 is:

- Men: approximately $108,000

- Women: approximately $79,000

That’s the median — meaning half of all Australians in that age group have less than those figures. And the gap between what most people have and the $168,000 benchmark is real. So if your balance is sitting below that mark, you’re in very good company.

The gender gap is also stark and worth naming. Women in their 40s typically have around 28% less superannuation than men the same age. This largely reflects the reality that women are more likely to take career breaks for caregiving, work part-time, or spend time in lower-paid roles. It’s a systemic issue — and it means women often need to be especially intentional about super strategies in their 40s.

The good news? The gap between where most people are and where they need to be is very close to being closed — especially with 20–25 years of compounding growth still ahead.

Why Most 40-Year-Olds Are Behind (And Why That’s Okay)

There are very good reasons why super balances are often lower than the benchmarks suggest they should be at 40. Life doesn’t happen in a straight line.

The Superannuation Guarantee (SG) — the compulsory amount your employer is required to pay into your super fund — has only been at 12% since 1 July 2025. For most of the past two decades, that rate was significantly lower. In 2002, it was just 9%. If you started your career when contributions were 9–10%, your earlier years contributed less to your super than they would today.

Career breaks for parenting, caring for elderly family members, studying, or health reasons all reduce the years of contributions going into your fund. Part-time work has the same effect. And for many Australians, super simply wasn’t front of mind in their 20s and 30s — which is entirely understandable.

Here’s the thing: your 40s are actually one of the best decades to play catch-up. You likely have a higher income than you did earlier in your career. You may have fewer years of high expenses ahead (think: a mortgage that’s partly paid down, kids who will eventually become financially independent). And you still have enough time for compound growth to do meaningful heavy lifting.

What Affects Your Super Balance at 40

Super balances aren’t just a function of how long you’ve been working. Several factors shape where you land:

- Your salary. The SG is calculated as a percentage of your ordinary time earnings, so a higher income generally means higher employer contributions. Someone earning $120,000 receives $14,400 per year in SG contributions (at 12%); someone earning $60,000 receives $7,200.

- Career breaks. Every year out of the workforce is a year without SG contributions. A two-year career break at 32 doesn’t just mean two years of missing contributions — it means those contributions never get to compound over the remaining decades.

- Multiple accounts. Many Australians still have multiple super accounts from different jobs, each quietly charging fees. Consolidating accounts can stop the fee drain and simplify your super strategy. (Check for lost super at the ATO’s online services through myGov.)

- Investment returns. The investment option you’re in matters significantly over long time horizons. A growth or balanced option historically returns more over 20–30 years than a conservative option, though with more short-term volatility. It’s worth reviewing whether your current investment option aligns with your timeline.

- Employer contributions above the minimum. Some employers offer to match additional contributions. If yours does and you haven’t taken up that offer, it’s one of the highest-return moves available.

Practical Ways to Boost Your Super in Your 40s

If you’re behind the benchmark — or simply want to maximise where you’ll land — here are some strategies many people in their 40s explore. These are general options, not personal recommendations; a financial adviser can help you work out which, if any, are right for your situation.

- Salary sacrifice. This involves asking your employer to direct some of your pre-tax salary into your super, rather than paying it to you as income. Because contributions go in before income tax is applied, salary sacrifice can be tax-effective for many people — though the benefit depends on your individual tax situation. All employer SG contributions and salary sacrifice amounts count towards the concessional contributions cap of $30,000 per year (2025–26 financial year).

- Carry-forward contributions. If your total super balance is below $500,000 and you haven’t used your full concessional cap in previous years, you may be able to “carry forward” those unused amounts and make larger contributions in a single year. This is particularly useful if you have had career breaks or periods of lower income. Unused cap amounts can be carried forward for up to five years.

- After-tax (non-concessional) contributions. Some people also choose to contribute from their take-home pay to super. These don’t attract the same tax benefit as salary sacrifice, but the money is then invested in a tax-effective environment.

- Super co-contribution. Lower-income earners who make personal after-tax contributions may be eligible for a government co-contribution of up to $500. Income thresholds apply and are updated annually.

- Consolidate your accounts. If you have multiple super funds, consider rolling them into one. Fewer accounts generally means fewer sets of fees — and fees compound just like returns do, only in reverse.

A Worked Example: Meet Sarah

The following example uses hypothetical figures to illustrate how extra contributions can affect long-term super outcomes. Assumptions are stated clearly. This is not financial advice.

Sarah is 40 years old and works as a nurse, earning $78,000 per year. Her super balance is $65,000 — below the median for women her age, partly because she took two years off when her children were young. She’d like to retire comfortably at 65, which gives her 25 years.

Assumptions: 7% annual net investment return (after fees and taxes within super), SG contributions at 12%, no changes to salary or contribution caps over time.

Scenario A — SG contributions only (no extra):

- Annual SG: 12% × $78,000 = $9,360

- Projected balance at 65: approximately $960,000

Scenario B — Sarah’s salary sacrifices an extra $400/month ($4,800/year):

- Total annual contributions: $14,160 (well within the $30,000 cap)

- Projected balance at 65: approximately $1,270,000

The difference? Around $310,000 — from adding just $400 per month in salary sacrifice over 25 years.

That extra $310,000 could mean the difference between a modest and a comfortable retirement, or between needing to draw on the Age Pension and having genuine financial flexibility in later life.

Of course, real-life outcomes will vary. Investment returns aren’t guaranteed, contribution caps may change, and individual circumstances affect every outcome. This example is illustrative only.

When to Get Advice

Super isn’t one-size-fits-all. The benchmarks are useful reference points, but they can’t account for your specific income trajectory, planned retirement age, property situation, family circumstances, or risk appetite.

Some situations where professional advice can make a real difference include:

- You’ve had significant career breaks and want to understand your options for catching up

- You’re uncertain whether salary sacrifice makes sense given your income and tax position

- You have superannuation in multiple funds and want to consolidate strategically

- You’re approaching a major life change — a new job, selling a property, a divorce, or an inheritance — that might affect your super strategy

- You simply want to know exactly where you stand and what a realistic retirement looks like for you

A financial adviser can model your specific situation and help you make decisions with confidence, rather than guessing.

Your Next Step: Book a Super Health Check

If reading this article has prompted the question “but what does this mean for me?” — that’s exactly the right question to be asking.

At Inspired Money, we offer a Super Health Check designed for people in their 40s who want a clear, personalised picture of where their super is at and what they can do to improve it. It’s a practical, no-jargon conversation with one of our financial advisers — focused on your goals, your timeline, and the specific steps that make sense for your situation.

Book your Super Health Check with Inspired Money →

Because the best time to take a look at your super was ten years ago. The second-best time is now.

This article contains general information only and does not take into account your personal financial situation, objectives, or needs. Before acting on this information, consider whether it’s appropriate for you and seek advice from a licensed financial adviser. Past performance is not a reliable indicator of future performance. All figures are based on publicly available data current at the time of writing (May 2026) and are subject to change.

Sources: ASFA Retirement Standard (December 2025 quarter); ATO Taxation Statistics 2022–23; ATO Key Superannuation Rates and Thresholds 2025–26; APRA Annual Superannuation Bulletin 2024–25.