Well, I came across the Theodore R. Johnson story when reading Tony Robbins, Money Master The Game, book a few years ago, but was reminded about the story when the office opened a conversation on how important compound interest is and equally how misunderstood it was.

So back to Theodore R. Johnson, he worked for UPS and never made more than $14,000 a year. After a 28-year career with the company, he retired in 1952 with $700,000 in company stock. He remained retired for 39 years while amassing a fortune of $70 million.

Johnson died at the age of 91 leaving much of his fortune to an education fund he established with his wife, for disadvantaged students attending small colleges.

70 Million…so how did he do it?

The internet and news are full of many stories about people retiring today worrying about if they’ll run out of money in their later years. So how was Johnson able to retire and grow his $700K into a $70 million fortune that will benefit many into the foreseeable future?

Simply….he took advantage of compounding!

Johnson shared Warren Buffett’s investment philosophy and was a buy and hold investor who purchased stocks and reinvested the dividends. A quick calculation shows Johnson achieved a compound annual growth rate of about 11.9% over the 39 year period of his retirement. Returns, S&P 500 over that same period 11.5%.

Johnson was a saver and took advantage of dollar cost averaging (purchasing stocks or managed funds on a scheduled basis, regardless of price or the economy) to purchase and amass UPS stock over his 28 year career with UPS, participating in any stock purchase program the company made available.

He took advantage of compounding, meaning he left much of his investment untouched and continually reinvested dividends on top of gains. He even had the added risk of being very heavily invested in UPS stock versus spreading his investments across multiple dividend paying companies. Investors today can easily invest in the entire market or the S&P 500 through low-cost index funds that can deliver similar long term returns with less volatility. Spreading your investment across hundreds of US companies doing business around the world reduces risk.

And….he started early,

He began investing as soon as he started working and continued consistently throughout his career.

…lived frugally,

After raising a family, Johnson and his wife moved to a two-bedroom unit in Delray Beach, Florida. From the outside, this looks like a pretty traditional retirement but when you look at some of the multimillion-dollar homes along the coast or river, you’ll see some future retirement stories that don’t end so well. Johnson was able to enjoy the same view and outdoor activities as some of these, less fortunate neighbors who had the need for waterfront property with boat slips and four-wheeled drive filled three-car garages.

…and took his time!

Amassing a $70 million fortune does not happen overnight. Johnson was patient and rode out some very difficult times in the US economy including wars, inflation, 70s oil embargos, and multiple recessions. His low cost of living helped him stay the course.

Remember taking time requires having time.

Johnson took care of himself with regular exercise, reaching the age of 91 and staying active. This time allowed the power of compounding to take effect resulting in the fortune he amassed that will benefit others.

He never stopped learning and doing.

Following his wife’s lead, he put together an education foundation late in his life that will now be funded indefinitely.

Don’t doubt it.

So you’re thinking, easy for Johnson, he had a long career with a successful company and probably had a pension he could live off of. What about people in today’s economy who don’t have these types of benefits and jump from job to job with little hope for a superannuation or company share plans?

Then there’s Ronald Reed.

A Vermont man who never graduated from college worked as a janitor and gas station attendant and amassed a fortune of $8 million. In 2015 he bequeathed much of that to a local library and hospital. How could someone of modest means working in today’s economy build such a fortune.

How did he get there, the answer is the exact same way Johnson did.

- He was a buy and hold investor who used dollar cost averaging to invest in US dividend paying stocks, taking advantage of compounding by reinvesting all dividends.

- He lived frugally but had enough money to enjoy visiting friends at local restaurants every day.

- He took his time. He lived to 92 and would rather walk a mile than pay for a parking spot. Walking pays dividends in other ways. Through his later years, he stuck with his investments through good times and bad including, recessions, tech bubbles, and the 2008 financial crisis.

- He never stopped learning and doing. He left over $1.6 million to the local library he loved so much. He studied investing and read the Wall Street Journal to keep up with companies he invested in like GE, AT&T and General Motors who’ve had some rough times of their own over the years.

Like Johnson, he left behind a large legacy, giving much of his fortune away to benefit others.

So what is the must read message here for the under 25’s?

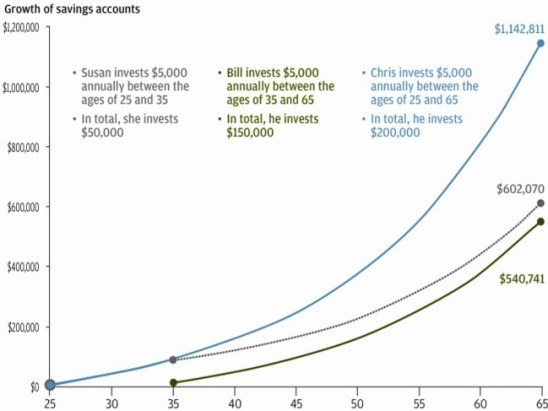

The message is to simply start early!. This gives all the other advantages of the plan the time to fall in place. These include compound interest, dollar cost averaging, dividends, and market growth. The simple chart shows even those who start early and then stop after as few as 10 years often end up with more than those who invest up to three times as much but get a late start. Those who end up ahead like Johnson and Reed did start early and stuck with it even through the toughest of times.

via Business Insider Compounding Example.

Susan invested $5000 annually between the ages of 25 and 35 only. Thanks to an early start her money had time to grow and compound. She ended up with more than Bill who invested three times as much as bill but got a later start at the age of 35. Chris ended up ahead of the others as he continued to invest continually throughout his working years.

Reference:

UPS Employee With a $70 Million Net worth?! Retiree Donates Fortune to Education

To book a session to review your wealth creation & retirement plans contact Conrad directly on 08 6222 7909 or book a meeting directly via his booking page.